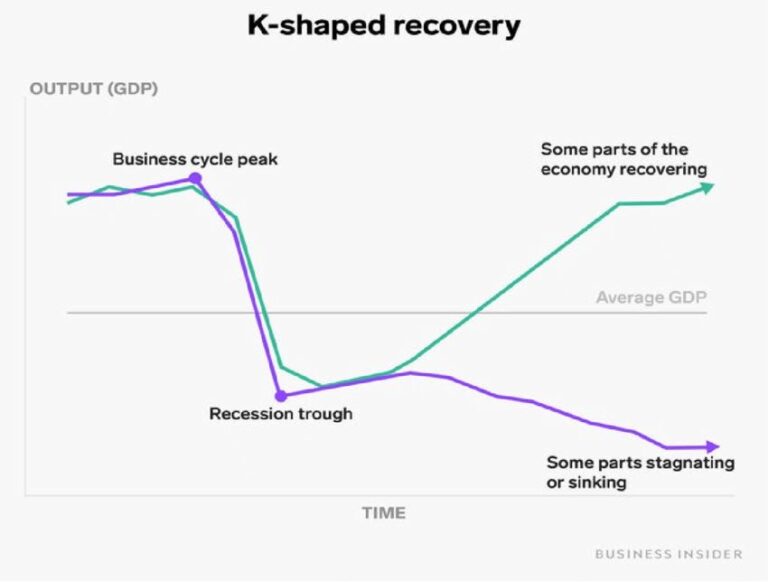

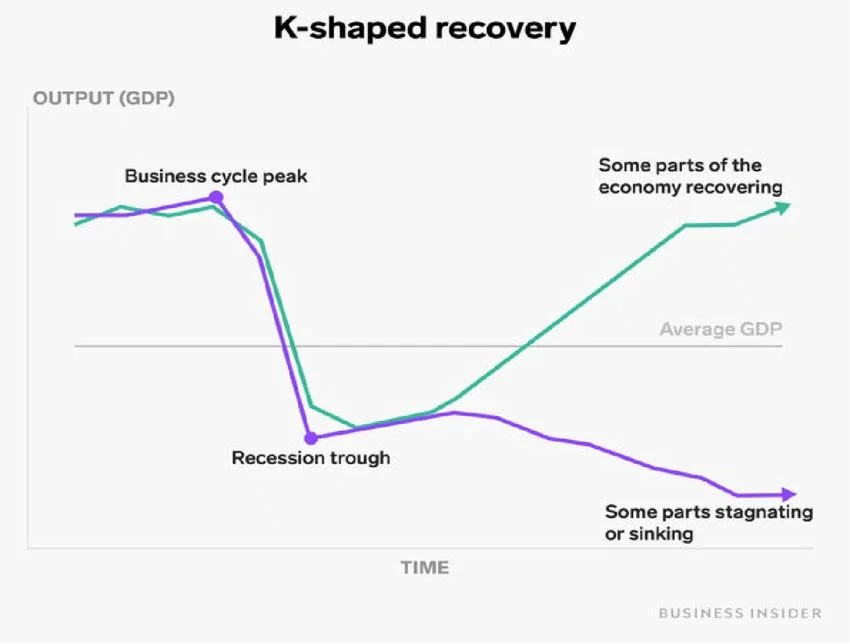

In every economic disruption, businesses don’t move together. They split. Some accelerate. Some stall.

That divergence is called the K-shaped recovery, a term popularized during the post-pandemic rebound and widely discussed by institutions like the @Federal Reserve and reported on by outlets such as @The Wall Street Journal.

But this isn’t just a macroeconomic headline. It’s happening inside manufacturing right now. And it’s accelerating.

What the K-Curve Looks Like in Manufacturing

The upward leg of the K:

- Manufacturers investing in automation and AI

- Companies reshoring strategically instead of reactively

- Firms tightening their ICP and walking away from bad-fit customers

- Shops that measure response time, quoting speed, and sales velocity weekly

- Leaders who treat marketing as a growth system, not an expense

The downward leg:

- Shops waiting for tariffs to stabilize

- Companies blaming workforce shortages without fixing training pipelines

- Businesses chasing every RFQ instead of profitable work

- Owners cutting marketing first

- Leaders frozen in uncertainty

Tariffs. Supply chain instability. Workforce gaps. Capital constraints. These pressures aren’t new. They’re just exposing operational maturity gaps.

The Hidden Multiplier: Strategic Agility

During my career working inside and alongside more than 25 manufacturers, I’ve seen this pattern repeatedly. In downturns, the strongest companies do three things:

- They narrow their focus.

- They double down on operational efficiency.

- They invest when competitors retreat.

During the reshoring wave, many shops scaled without strengthening systems. Now, we’re seeing the consequences: undercapacity, strained labor pools, and margin compression.

The companies on the upward leg of the K aren’t necessarily bigger. They’re clearer on:

- Ideal customer

- Core competencies

- Pricing discipline

- Data visibility

- Tech stack alignment

- Sales, operations, and marketing alignment

That clarity compounds.

The Tariff Trap

Tariffs create volatility. Volatility creates hesitation. Hesitation widens the K. The manufacturers winning right now are not trying to predict policy. They’re building resilience:

- Diversifying supplier geography

- Strengthening North American trade relationships

- Investing in automation where labor is constrained

- Building skilled pipelines instead of poaching talent

- Using AI to compress admin and quoting cycles

They understand something critical: Uncertainty punishes the unfocused.

Workforce Isn’t the Problem. Strategy Is.

I’ve worked with welding shops, machining operations, industrial distributors, and construction trades. The labor conversation is real. But the deeper issue isn’t “no workers.” It’s:

- No structured training

- No documented processes

- No employer brand

- No clear growth positioning

The upward side of the K builds systems that make workforce scalable. The downward side relies on heroics. Heroics don’t scale.

Holistic, Systemic Growth Strategy Is the Separator

Here’s the uncomfortable truth: In manufacturing, market maturity often determines which side of the K you land on. Companies that:

- Define who they serve

- Say no to low-margin work

- Build authority in a niche

- Align sales and marketing around profitable segments

- Measure inquiry-to-human-response time

Grow. Companies that “wait until things settle down” shrink. I’ve seen this firsthand scaling startups and established manufacturers alike. In volatile markets, clarity beats capacity.

The Question Every Manufacturer Should Ask Right Now

If the economy stays uncertain for 18 more months:

- Are you positioned to gain share?

- Or are you positioned to survive?

The K-curve doesn’t care about tenure, legacy, or equipment size. It rewards discipline, speed, and strategic focus. And the gap is widening.

If you’re a manufacturer navigating tariffs, supply chain shifts, workforce constraints, and growth pressure, now is not the time to freeze. It’s the time to decide which side of the K you intend to operate on. Because in this cycle, the middle is disappearing.